Graduate Management Accountant (GMA) Program Overview

Entry Requirements

GMA Program Overview

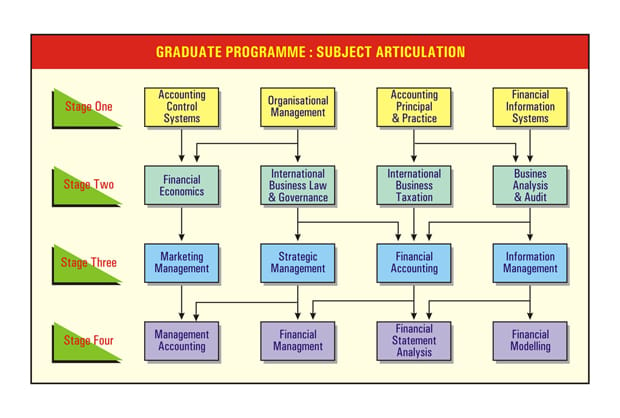

There are four stages in the Graduate Member programme, each stage requiring the passing of four subjects. A detailed list of the subjects is provided in Figure 2, and Figure 3 below shows the articulation process with each stage leading naturally to the next one, and building on what has been learned in previous stages. The GMA program has a university entry level (high school certificate) entry requirement.

The GMA Conversion Program

To join as a Graduate Management Accountant (GMA) via the GMA Conversion Program, the student must complete Stage 4 of the graduate program (4 subjects).These subjects may be undertaken directly (without completing Stage 1 to 3) by holders of a degree in any discipline or a professional qualification in any discipline other than accounting. These subjects are taught at the honours/masters level.

Partially Completed Studies

Students who have partially completed programs at universities, recognised professional bodies, and other educational and training establishments may apply for credit on a subject-by-subject basis. Further, it is one of the objectives of the Institute to accredit Graduate Conversion Programmes offered to non-accountants to convert to accountancy at recognised universities and educational bodies. Holders of Graduate Diplomas in Accounting and above, will be thus eligible for Graduate membership in the Institute.

The Institute’s own Graduate Conversion Programme, consists the four subjects of Stage 4 in Figure above, taught at a University 4th Year (Honours/Graduate Diploma) level.

Certified Accounting Technician Program (GMA Program Stage 1)

Registered Cost Accountant Program (GMA Program Stage 2)

Registered Business Accountant (GMA Program Stage 3)

Graduate Conversion Program (GMA Program Stage 4)

- Professor Ian McPhee talks on the “Reminiscences of an Auditor General in Advancing the Profession”

- Professor Brett Sutton talks on “Existential Threats and Complex Systems”

- Dr. Angie Bone talks on “Planetary Health Economics in Sustainable Value Creation”

- Senator Barbara Pocock talks of the “Abuse of Trust at PwC and the Role of Journalists and Whistle-Blowers”

- Prof Janek Ratnatunga on “Future Proofing Indonesian Companies”

Stay In Touch